The below is a high level introduction, all elements are subject to change.

Summary

The following outlines established and emerging issues within the governance and treasury management of Kusama and introduces a new financing strategy, structure and partnership with ABO Digital who have extensive experience in providing flexible, innovative and compliant financing for publicly listed companies.

This financing is especially useful in highly experimental and R&D heavy domains - for example bio-tech - where listed entities prefer consistent and patient capital allocation structured as a facility that can be drawn down as and when required and timing in line with positive news flow, rather than committing to more expensive capital when shares may be underpriced.

We believe the model and the strategy and structuring that it brings can address many of the recurring issues within the ecosystem, better aligning the collective interests of the network in a way that has so far proved impossible and providing the necessary stable foundations for Kusama to deliver on its long promised mandate to create chaos.

Background

Currently venture capital investors seed projects at the earliest stages in a manner comparable to startups and benefit from a quick path to liquidity through token listings, where opaque exchange operations, market makers and trading expertise offer them a comparative advantage over retail investors drawn into initial hype who then act as exit liquidity for early investors.

These investors benefit primarily from the first wave of hype where massive returns mean they can deliver huge returns to their LPs before any meaningful network adoption, creating a short term mindset that flips profits from project to project, taking advantage of a lack of regulatory oversight.

As the relative adoption of crypto-networks attests, taking stake in a network through singular large ticket events ahead of launch, works well for returning investors capital quickly, but not for growing highly complex, experimental and R&D focused public networks that require consistent, patient and committed capital allocation over many years.

Current challenges

Kusama and Polkadot’s crowdloan marketing mechanics and the resulting independent parachain economies are products of this same speculative cycle and therefore face the same challenges as the wider crypto industry when it comes to delivering meaningful adoption:

-

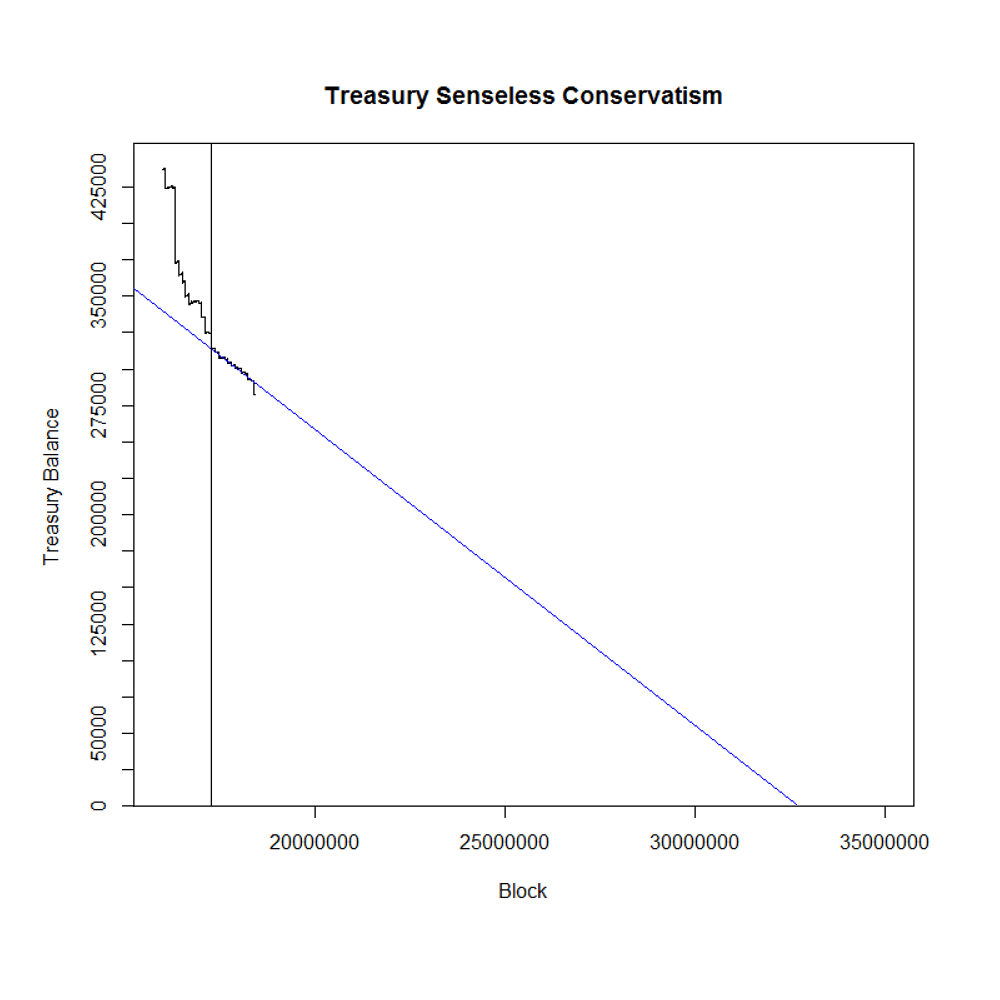

Even though the treasuries may control millions when valued in fiat terms, their actual spending power is constrained by the requirement of funded teams to sell KSM/DOT for working capital on an ad hoc basis, which creates sell pressure, thus reducing the available capital over time in unpredictable ways.

-

Without a consistent baseline, each team prices and values their contributions independently, before proposing and receiving funds whose relative value varies widely on receipt of payments and then further upon inconsistent and inefficient disposal to stablecoins leading to spectacular variations in funds eventually received by teams.

-

Proposed solutions to getting proposers stablecoins include an Asset Hub exchange pallet (statemint DEX) that does not address the ad hoc nature of fund disposal into working capital and is not an efficient way to dispose of large amounts of a network token since the treasury is likely the primary LP.

- To further complicate the picture, the lack of any corporate entity or clear governance structures associated to DAO treasuries or the collectives that would shape the future of the network opens up members to potential legal peril and ensures large holders prefer to vote anonymously or abstain from interaction all together, leaving network’s adrift with low participation rates and a lack of oversight. Given regulatory headwinds, the worst case scenario is much of this capital may become increasingly unspendable as the risks of not being compliant mount.

Issues that steadily degrade culture

Considered together, this fragmented approach to network governance, treasury management and project funding inevitably leads to circular and irreconcilable arguments between token holders and contributors who operate under constantly shifting conditions which makes long or even medium term strategic planning impossible.

The arrival of the HACN activist token holders who are collectively blocking treasury spending for proposals without any perceived strategic foundations has shone a light on a number of issues with scattergun spending.

However whilst voting Nay offers some general policy guidelines and gives the community pause for consideration, it does not offer a definitive path forward - leaving things in limbo.

On-chain decision making in its current form is an incredibly blunt instrument - referendums are either yes or no, therefore at the core of developing new strategies to resolve tensions must be an understanding of the primary mechanism to consistently and predictably align interests in a network of adversaries:

How the structure works

Given the highly volatile and organic development of public blockchains through market cycles, it makes more sense to have access to a guaranteed draw-down facility that can be tapped as and when it is required, ensuring tokens are sold at optimal moments.

Rather than selling tokens in one transaction, a pre-agreed funding facility (c. $10m for Kusama) is agreed and then tokens are delegated to a proxy of the treasury and are sold at the discretion of a group of stewards who retain the right, but not the obligation to sell to the investor in a series of tranches of c. $1m that is received directly into a series of treasury accounts.

Importantly these accounts are spendable without changing existing governance processes and will not impact the continuing accrual of KSM to the core treasury account.

Curators experienced in capital management, regulation and financing represent the best interests of the network and are incentivised through transparent mechanisms aligned to the best interests of token holders.

These curators establish and manage regulatory compliant processes through a legal vehicle, sign legal agreements with the investor and dictate timing of token sales based on optimising for market conditions and network development within a commitment period of c. 36 months.

This approach has the further benefit of evolving scattergun treasury funding across domains into focused tranches established to pursue more considered directions.

This allows more structured budgeting as the collective’s attention and talent are coordinated towards developing more strategic and less reactive innovation initiatives whose impact can be assessed across an evolving strata of qualitative and quantitative measures.

This approach addresses many issues with current treasury operations:

- more strategic, accountable and patient approach to network financing

- removes uncertainty for teams in terms of the funds they eventually receives

- addresses tax and invoicing issues for teams when interfacing with the treasury.

- removes inconsistent and sub-optimal sell pressure as teams convert network tokens into working capital

- sets a more consistent baseline for assessing future ROI of treasury spending.

- establishes compliant processes by marrying on and off-chain governance structures to ensure these are not enforced by courts.

Political power remains with the collective

All of this is conceived to not take control away from the collective, but to establish some basic oversight, compliance, administration and strategic foundation.

In the end, when these funds are deployed and for what purposes will remain at the ultimate discretion of the voting public.

Overview of the process

The below gives a high level outline of the process - this is subject to change.

Benefits of the model include:

- A firm commitment from the investor to purchase tokens allowing curators to sell token as funds on an as-and-when basis.

- Curators maintain control over the timing and the number of tokens that are sold to the Investor, enabling it to determine when capital will be raised and at what price.

- Lower cost of capital than other forms of fund raising, as the investor bears less risk – the structure can be a steady source of cash that can be used to fund ongoing working cap needs, avoiding raising capital up front at an unfavourable valuation.

- A quick and efficient way of taking advantage of positive news flow and momentum in the tokens to raise cash that is tried and tested in public markets.

- Investors will be hedging their position by selling borrowed tokens but doing so only at a slight discount to the TWAP to remain “in-the-money” as well as keeping its daily volume participation close to 10%. This results in minimal selling pressure.

- The increase in trading from this facility as well as the announcement will help boost liquidity. Execution and custodian provider can also provide market-making services to help boost liquidity further and guarantees best execution at the TWAP.

Why this matters now

A phased approach

Though the concept is relatively simple on paper, the move from a purely off-chain structure to a hybrid on/off-chain structure makes this is a highly complex process without precedent as far as we are aware.

As a result we will be breaking down the project into a series of stages to ensure continuing transparency, accountability and compliance for all involved.

This staggered approach will also enable the wider community to learn, contribute and have their voices heard.

With treasury spending politics absorbing a huge amount of the ecosystem’s attention, it is also worth noting that this is just one type of funding, over time we expect that a more fluid and balanced innovation process will evolve, allowing ideas and talent to be supported through a more structured cycle that addresses current issues with the sustainable financing of public goods more generally.

A collective endeavour

We are bringing together a collective of well known ecosystem participants and new faces to bring this initiative together

Decent Partners have worked previously with ABO Digital’s parent company Alpha Blue Ocean and have extensive experience in project financing, network development, capital markets, fund management and legal and compliance.

Next steps

We will be hosting an introduction to the initiative with the team and ABO Digital in the following weeks as part of Chaos Sessions.

This introduction will allow us to outline our current approach to the phases involved, the challenges and issues to address and the opportunities for members to meaningfully contribute to what we hope will set a new standard for DAO financing across the industry and provide much needed foundations for the ecosystem to deliver on its next phase of focused innovation.

In the mean time, please share any questions here and we will fold them into the discussions.

Related reading

- A Better Treasury System

- Discussions on improving the current treasury spending/management mechanism

- OpenGov on Polkadot: Reflecting on the Payment Issues from Kusama

- Collective-Based, Multi-Asset Treasuries(Discussions on improving the current treasury spending/management mechanism)

- VAT on Services in/to the ecosystem

- Legal status of Kusama / Polkadot DAOs

- Kusama Treasury Follow-up Analysis: Continued Budgeting Incompetence