This post extends the analysis first outlined in Kusama treasury annual spending analysis - 2020 > 2023 (june), @asteeber’s Kusama Treasury Follow-up Analysis: Continued Budgeting Incompetence and the ongoing conversations in Adjusting the current inflation model to sustain Treasury inflow

Overview

Kusama is 3 years old, so it is worth considering what has been learned in that time, what historical insights may be surfaced from existing data and how this can inform future strategies as the ecosystem moves from an evolving coretime loan model, to a coretime sales model.

This post includes data from a coretime lease and treasury spendng analysis - its purpose is to offer a starting framework to get people to see the network differently.

The underlying model

The Twitter thread version

For those who like your analysis in tweets.

Key points:

-

Parachain auction speculation continues to hide many sins, creating valuations and treasuries that seem secure and sustainable, but that do in fact exist precariously - held up more by hope than reality.

-

Historical data from coretime leases can help us model future expectations around coretime pricing and income for both Instant and Wholesale offerings and allow us to to better plan future scenarios.

-

Current and historical spending strategies are detached from the fundamental value drivers of the network and its corespace product offering and as well as having zero impact, are entirely unsustainable in their current form.

-

Treasury spending should be focused on developing public good strategies that directly impact the demand for coretime as a raw material, funding teams transforming it into useful coretime resources.

Coretime loans vs coretime sales

The primary historical demand driver of $KSM has been through slot auctions and the creation of independent networks that leverage a shared security model to bootstrap their token economies.

In this model, customers of the network’s primary product of secure blockspace, use either their own funds, or those loaned by contributors to lease year long slots.

Although branded as parachain leases, it is useful to think of this paradigm through the lens of the new language as bulk annual coretime leases.

We can define the parameters of a lease in the following way.

| Coretime lease | ||||

|---|---|---|---|---|

| Period (days) | Periods | Duration (days) | Blocktime (seconds) | Blocks per lease |

| 42 | 8 | 336 | 12 | 2419200 |

The customers driving coretime lease demand are called parachains and we can understand the basic parameters in the following way, with total KSM locked acting as a surrogate for bulk coretime pricing.

| Coretime demand | |||||||

|---|---|---|---|---|---|---|---|

| Lease begins | Lease ends | Number | Parachain | Funding type | KSM bond | KSM price | Bulk price |

| 15-Jun-21 | 15-Jun-22 | 1 | Karura | Crowdloan | 501138 | $420.00 | $210,477,960 |

Coretime leases and opportunity costs

Since the coretime lease model relies on KSM being locked and then unlocked when the slot finishes. As a result, teams or contributors - the customers of coretime leases have their funds returned, and are therefore only sacrificing the opportunity cost of their KSM.

Since KSM locked in coretime leases is not staked, the simplest way to value this opportunity cost is in the staking returns a holder is forgoing which for Kusama is approx 10% pa.

Since coretime sales accrue to the network treasury rather than being returned to a customer, the opportuntity cost is replaced with a direct cost.

Coretime income

There are two proposed sales models for coretime:

-

Wholesale: Selling 4 weeks of “coretime” per month. This coretime can’t be assigned/used directly.

-

Instant: Similar to a parathread, this involves a continuous sale of “coretime” for immediate use.

Using coretime leases to benchmark coretime sales

Using previous parameters for coretime leases allows us an imperfect but useful comparison to track the transition from opportunity costs, to direct costs, valuing the Kusama’s primary product in the process.

We can take Karura’s example to model a coretime lease equivalent for wholesale and instant pricing - this was the most expensive coretime offered.

| Coretime equivalent | |

|---|---|

| Instant - price/block | Wholesale - 4 weeks |

| $87.0031 | $17,539,830 |

We can see the latest slot 93 was secured by Parathread 2274 at the following rates:

| Instant - price/block | Wholesale - 4 weeks |

|---|---|

| $0.0012 | $239 |

By aggregrating all of the historical data for coretime leases to date, we get the following results:

(note blended refers to the average/total of each year, whilst all time is an average/total of individual coretime leases).

| Kusama network history | All time | 2020 | 2021 | 2022 | 2023 - July | Blended |

|---|---|---|---|---|---|---|

| Kusama network value | ||||||

| TWAP | $127 | $35 | $381 | $61 | $30 | $127 |

| Coretime loans | ||||||

| Lease total | 3,436,253KSM | 0KSM | 2,792,013KSM | 595,831KSM | 48,409KSM | 3,436,253KSM |

| Lease average | 36,949KSM | 0KSM | 186,134KSM | 7,987KSM | 1,614KSM | 48,934KSM |

| Annual coretime loan demand | ||||||

| Bulk loan total | $1,182,193,973 | 0 | $1,083,068,026 | $97,620,456 | $1,505,491 | $295,548,493 |

| Bulk loan average | $12,711,763 | 0 | $72,204,535 | $528,516 | $50,183 | $18,195,808 |

| Coretime pricing | ||||||

| Price / block equivalent | $5.2545 | 0 | $29.85 | $5.2545 | $0.0207 | $8.78 |

| 4 Weeks wholesale equivalent | $1,059,314 | 0 | $6,017,045 | $169,480 | $4,182 | $1,547,677 |

Some charts

Now lets zoom out and look at the big picture.

Let’s begin with KSM price change over the 3 year period of parachain auctions. Note the vertical axis is on a log scale, which allows us to bring together data across a large spread.

For every one value of y, the value of x will increase by a factor of ten.

Now lets see the demand for KSM via the amount locked up in slots.

And then lets consider the total bulk price of these coretime leases.

Treasury spending

As noted previously, Kusama’s common good treasury has spent c. $22m in the past 3 years covering a range of domains.

| Year | 2020 | 2021 | 2022 | 2023 | Total |

|---|---|---|---|---|---|

| Costs | |||||

| Wallets | $94,034 | $600,985 | $936,762 | $207,749 | $1,839,530 |

| Development | $491,659 | $1,218,280 | $4,616,067 | $2,346,304 | $8,672,310 |

| Education | $26,987 | $330,999 | $2,208,839 | $661,728 | $3,228,553 |

| Art-Experiment | $141,088 | $5,670 | $39,800 | $12,018 | $198,576 |

| Events | $0 | $51,743 | $807,492 | $231,753 | $1,090,988 |

| DEX liqudity | $0 | $0 | $4,740,000 | $0 | $4,740,000 |

| Maintenance | $3,470 | $146,114 | $1,391,633 | $364,064 | $1,905,281 |

| Totals | $757,238 | $2,353,790 | $14,740,593 | $3,823,616 | $21,675,237 |

Since domains are categorised through subjective rather than objective means, the boundaries of each area remains unclear, in flux and open to interpretation.

When it comes to assessing the effectiveness of spending, each proponent presents, assesses and reports their own KPIs, although in many cases there is no reporting.

In general, the overall motivation is to generate awareness that will then result in some form of on-chain impact further down the road, though what this on-chain impact might be is rarely if ever discussed.

Individualism, Collective intelligence and Tragedy of the Commons

For voters wishing to make educated decisions in the public benefit, their assessments trend towards either personal interests and popularity contests.

When it comes to personal interests, voters with a specific expertise may be great at assessing the quality of a proponent in their specialist area, but poor judges when considering anything outside.

On the popularity contest side, the nature of token based communities trends towards tribalism - with previously funded teams afraid to vote against projects, for fear of losing support when the time comes to present new funding requests.

At the same time emerging contributor token-ocracy binds groups together to defend and extend their own common interests, but at the expense of a collective common good.

The compounding effect of this process is the collective becomes ever more divided, ineffective and wasteful - an entirely predictable tragedy of the commons that all token based treasuries are headed towards.

The tragedy of the commons is a metaphoric label for a concept that is widely discussed in economics, ecology and other sciences. According to the concept, if numerous independent individuals should enjoy unfettered access to a finite, valuable resource e.g. a pasture, they will tend to over-use it, and may end up by destroying its value altogether. To exercise voluntary restraint is not a rational choice for any one individual - if he did, the others would merely supplant him - yet the predictable result is a tragedy for all. - Wikipedia

What is the Kusama treasury for?

Despite the subject of so much attention, debate and argument, very little time is given to questioning the fundamental purpose of the common good treasury - and shared network resources in general.

Instead people’s short term focus tends to be on seeing the treasury as a pot to be spent on relatively arbitrary domains, whose relevative importance ebbs and flows depending on who is being asked, with little or no thought given to the primary demand and value drivers of the network.

With the arrival of coretime sales, we finally have a more concrete focus on the primary business that Kusama is in and therefore a way to focus attention, strategies and spending over the long term.

Setting coretime income expections

Objectively speaking, the primary driver of coretime leases were parachain auctions.

Demand was bootstrapped by crowdloans, with expectations of a new token, with no direct value accrual to the main network, the primary motivation for the speculative frenzy.

With teams now preferring to Self Fund rather than Crowdloan, we are beginning to get better signal as to the actual value of coretime in Kusama, since the speculative benefits have receded.

When we remove crowdloans from the picture, this is the current status of 2023 coretime lease demand when considered through the lens of coretime sales pricing structures for self-funded projects.

| Coretime pricing equivalent | |

|---|---|

| Instant - price/block | Wholesale - 4 weeks |

| $0.0131 | $2,639 |

When we use the data to calculate potential coretime income for 2023, we get the following:

Total income: 25306 KSM / $759,983

Remember coretime sales is a direct cost, whereas coretime leases are an opportunity cost.

In the absence of new demand drivers, this is likely the upper bound of income for Kusama.

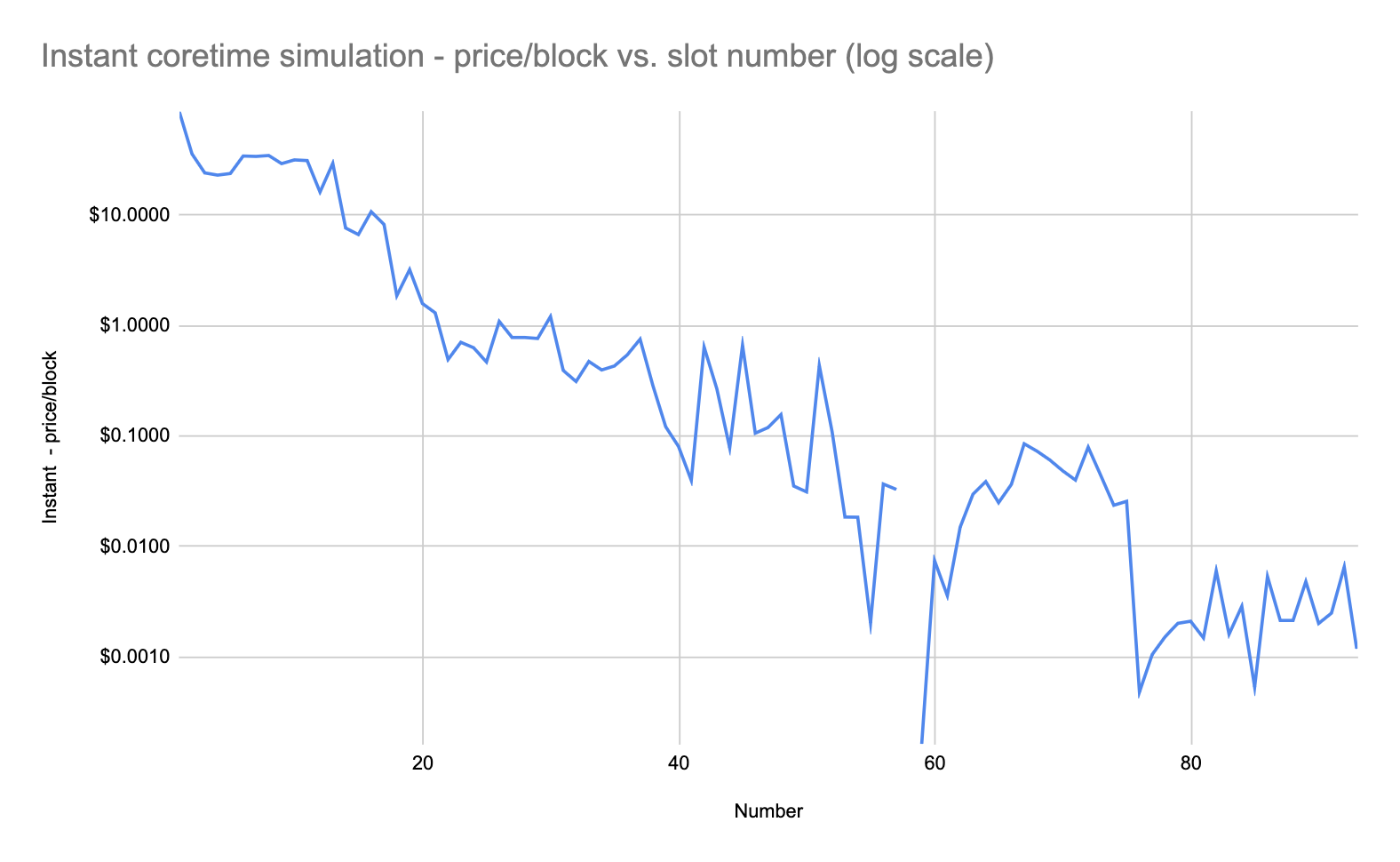

A few more charts

Using historical data to simulate Instant Coretime

Using historical data to simulate Bulk Coretime - 4 week periods.

Treasury ROI

When we focus our attention on the core business of the network, we can more easily assess the value of treasury spending to date.

Since demand for coretime leases has to date been driven by auctions, the ROI on treasury spending in terms of driving direct demand for corespace can be written down to 0.

| Kusama network history | All time | 2020 | 2021 | 2022 | 2023 - July | Blended |

|---|---|---|---|---|---|---|

| Kusama network value | ||||||

| TWAP | $127 | $35 | $381 | $61 | $30 | $127 |

| Coretime loans | ||||||

| Lease total | 3,436,253KSM | 0KSM | 2,792,013KSM | 595,831KSM | 48,409KSM | 3,436,253KSM |

| Lease average | 36,949KSM | 0KSM | 186,134KSM | 7,987KSM | 1,614KSM | 48,934KSM |

| Annual coretime loan demand | ||||||

| Bulk loan total | $1,182,193,973 | 0 | $1,083,068,026 | $97,620,456 | $1,505,491 | $295,548,493 |

| Bulk loan average | $12,711,763 | 0 | $72,204,535 | $528,516 | $50,183 | $18,195,808 |

| Coretime pricing | ||||||

| Price / block equivalent | $5.2545 | 0 | $29.85 | $5.2545 | $0.0207 | $8.78 |

| 4 Weeks wholesale equivalent | $1,059,314 | 0 | $6,017,045 | $169,480 | $4,182 | $1,547,677 |

| Treasury spending | ||||||

| Domains - awareness | $21,675,237 | $757,238 | $2,353,790 | $14,740,593 | $14,740,593 | $32,592,214 |

| Directions - impact | 0 | 0 | 0 | 0 | 0 | 0 |

| Total costs | $21,675,237 | $757,238 | $2,353,790 | $14,740,593 | $14,740,593 | $32,592,214 |

| Treasury ROI | ||||||

| Direct coretime demand | 0 | 0 | 0 | 0 | 0 | 0 |

| Common good return | -$21,675,237 | -$757,238 | -$2,353,790 | -$14,740,593 | -$14,740,593 | -$8,148,054 |

Coretime as a public asset → Coretime as a public resource

So if the common good treasury is not for funding arbitrary domains, what might it be for?

By beginning to focus attention on the metrics that really matters - coretime demand and price, we can begin to build cohesive strategies to make sustained impact.

If we begin by understanding that corespace is a raw material - computation.

This computation has a cost that is currently defined primarily through indirect means, however we can still value it using simple methods and in turn begin to structure treasury spending in ways that can directly impact coretime demand.

Further thoughts

This work is once again designed to prompt questions, challenge orthodoxy and push people to understanding that the challenges Kusama and Polkadot face are existential in nature, despite the distracting nature of token valuations.

For those expecting coretime income to save the day, it is worth considering the numbers and the trajectory the networks are on in terms of pricing power.

Hope for the best, plan for the worst.

The spreadsheet is there to be critiqued, copied, evolved and amended. Do your worst.